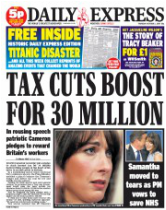

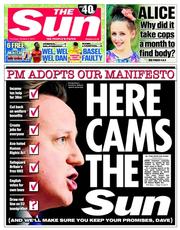

Crunching Cameron's tax-cut numbersThursday 2 October, 2014 For once, Cameron got exactly the headlines he wanted this morning: tax cuts for 30m people. This was his reward for a confident - even "fizzing" speech - to round off the Conservative conference.

Vote for him next year and by 2020, people earning £50,000 a year would not have to pay higher-rate tax; people on the minimum wage who worked 30 hours a week would pay no tax at all. Zero, zilch. The promise would, we were told, cost £7.2bn to implement. But we were not told where that £7.2bn would come from. Much play was made today of that gap in the rhetoric - Ed Balls threw back at the Prime Minister his own remark that a promise was worthless unless it was accompanied by details of how it would be financed. Meanwhile, estimates of the benefit of the tax band changes ranged from £160 to £2,167. The Government itself said that someone on £50,000 a year would be £1,313 to the good. Journalists are not known for their numeracy, so most papers didn't attempt to analyse the figures. The Independent and the Times went so far as to ask City experts to run them through a calculator, but that was about as far as it went. For the most part, coverage was mood music - and a very good mood the Sun, Express, Telegraph and Mail were in, too. There are no mathemeticians at SubScribe, either. But it seemed worth grabbing an envelope, pencil and a compound interest calculator to see what we could discover. Just like in our O levels, we are going to try to show our workings - if only so that those with greater numerical felicity can point out the errors along the way. The first problem we encounter is George Osborne's freeze on benefits - in this case we are concerned with working and child tax credits. The two-year freeze is to follow a 1% increase, so it should take us through to 2018, more than halfway through the next Parliament. To complicate things futher, a universal benefits/credits system is being piloted in some parts of the country. So please bear with us. Some basic figures 2010

Low-wage family Take a couple with a school-age child where both partners were paid the minimum wage. If one works 40 hours a week and the other 20, their annual family earnings would be around £18,000. Their finances would look something like this: Income £12,000 + £6,000 = £18,000 Tax £1,106 National Insurance £720 Tax credit £1040 Total income £17,214 (*We are deliberately ignoring child benefit throughout) Middle manager Now let's look at someone earning £50,000 a year (someone so short-sighted that they do not contribute to a pension fund or do anything else to disrupt the standard PAYE calculations) Income £50,000 Tax £9,932 National Insurance £4,260 Take-home pay £35,808 Moving on to today, here's how things have changed: 2014

Low-wage family The household budget for the minimum wage couple with the school-age child is now: Income £13,000 + £6,500 = £19,500 Tax £600 NI £605 Tax credit £1,362 Total income £19,657 Middle manager For the £50k a year employee, who still isn't paying into a pension, the figures are: Income £50,000 Tax £9,627 NI £4,260 Total income £36,142 Looking ahead to the end of the next Parliament is tricky. We don't know what will happen to the tax credit regime or to National Insurance. Nor do we know where the minimum wage will be set. Ed Miliband has promised to take it up to £8, and it seems fair to assume that the Tories won't match that. Cameron has spoken of "working towards" £7. Combining his promises that no one working 30 hours on the minimum would pay tax and the thresholds of £12,500/£37,500, he appears to be giving himself enough leeway should the minimum reach the Miliband level. So for the sake of argument, we'll be generous and assume a rate of £8. The ceiling for 12% NI payments is in line with the 40% tax threshold, but the allowance before contributions become payable is smaller. If the ceiling were to retain its link with the higher tax band, payments would need to start at around £8,000 in order to give the £50k earner the £1,313 benefit cited by the Government. Heaven knows what will happen to tax credits - if they will even survive - so we'll work on the basis that they are frozen at today's levels, which should offset any shortfall in the minimum wage. That would leave us making the following assumptions: 2020

Low-wage family The minimum wage couple's family income would now look like this (remember Cameron's promise was to people working 30 hours a week, one of our pair works 40; the Prime Minister also said that they would pay no tax; he didn't mention national insurance): Income £16,000 + £8,000 =£24,000 Tax £700 NI £960 Tax credit £422 (at current levels) Total income £22,760 Since no one was trumpeting such increases for the low paid, it seems reasonable to assume that the minimum wage will not hit £8. So let's do the sum again at £7: Income £14,000 + £7,000 = £21,000 Tax £300 NI £720 Tax credit £1043 (at current levels) Total income £21,023 Middle manager On to the £50,000-a-year worker and it looks like this: Income: £50,000 Tax: £7,500 NI: £5,040 Total income £37,460 That all seems fine and dandy. But there are a couple of pointers to remember.

And there's another element that comes into play with all this: inflation. The inflation rate for 2010 was 3.3%, for 2011 4.5%, for 2012 2.8% and for last year 2.5%. It is running at about 2% this year. If the personal allowance and tax thresholds had risen in line with inflation over the period of the coalition government, the basic allowance would now be £7,605 and the higher-rate threshold £42,539. That means you would already have to earn £50,144 to have to pay the 40p tax. But the fact that the personal allowance has far outstripped inflation is obviously better news for the lower-paid. As it is, the family on the minimum wage when the coalition came to power have pretty much kept pace with the cost of living over the past five years. Their 2010 income would be worth £19,332 today, slightly less than their present total. But looking to the future, the £21,023 they can expect in 2020 (if inflation stays constant at 2%) will be worth only £18,667 in today's money. If the rate went up to £8 an hour they'd be about £600 better off than today in real terms. As for our middle manager, the £35,808 he or she was taking home at the end of 2010 would have had the buying power of £40,215 today. And if inflation remains constant at 2% to the end of the next parliament, their expected £37,460 will be worth only £33,263 in today's money. Suddenly nobody looks better off. |

|

This entire enterprise was malicious and misconceived, and has resulted in women losing a valuable voice in government. Newmark founded Women2Win with Baroness Jenkin in 2005. That's nine years of campaigning to help women advance in the macho world of Westminster. Did the Mirror's freelancer think that Newmark was in it only to find young blondes willing to take their clothes off?

Editor's blog

Journalistic sting operations tend to be targeted and, whatever the protestations of the alleged victims and their apologists, often illuminate and amuse the rest of us while embarrassing the stung. I have no sympathy for senior politicians who display unacceptable naivety and get caught out.

The Newmark saga shows an imperfect, supposedly free, robust and knockabout press doing its work - Richard Dixon Style Counsel |

Please sign up for SubScribe updates

(no spam, no more than one every week or two)

|

|

|